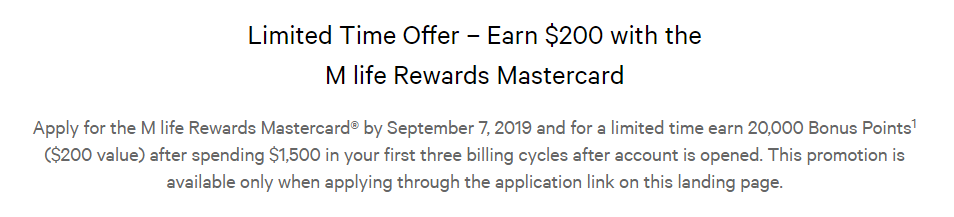

Update 8/26/19: Bonus has been increased to 20,000 points after $1,500 in spend. No longer comes with the free night though. I think it makes more sense to wait for a free night offer to return.

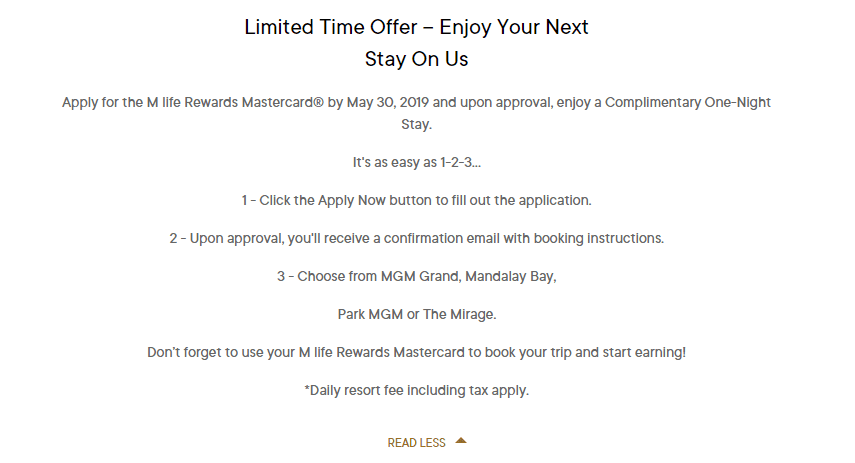

Update 4/17/19: They are currently offering a free night that can be used at MGM Grand, Mandalay Bay,Park MGM or The Mirage. This is in addition to the 10,000 points after $1,000 in spend they normally offer as well. Hat tip to reader Yoshi

M life Rewards has just released their M Life Rewards Mastercard, this new card is issued by First National Bank of Omaha. In this review we will look at the pros & cons of this card and see if it’s worth applying for. Keep in mind unlike other credit cards you need to be 21 years of age to apply for this (as this is a requirement of the M life program).

The following are the main marketing points for this card:

It’s no good knowing how many points this card earns unless we know what these points can actually be used for. As mentioned in the marketing material these points can be redeemed for ‘FREEPLAY® or Express Comps™’. If you’re anything like me, you probably have no idea what those mean.

1 Mlife point is equal to 1¢, regardless of whether you use it for an express comp or freeplay (although this obviously isn’t nearly as good as cash). This means the sign up bonus is worth a maximum of $100 and the card earns at a maximum of 3% on M life destinations and 2% on gas & supermarkets and 1% on all other purchases.

It’s possible to earn more with other credit cards for gas purchases, supermarket purchases & non bonused spend as well. Also keep in mind you need to redeem a minimum of 1,000 points ($10) when using them for Express comps. There is also a cap of $5,000 for express comps (or $10,000 if you have Noir status).

The only other real benefit this card offers (apart from the sign up bonus and bonus categories mentioned above) is status. You get the following:

Normally Pearl status requires you earning 25,000 tier credits. It’s the second lowest status (Sapphire is the base status anybody receives when signing up). It comes with the following benefits:

There are three other status levels that are higher than Pearl, their names followed by tier credits required and benefits are:

The benefits aren’t amazing on any of the tiers, unless you’re gambling a lot and earning a lot of points/express comps in which case the bonus multipliers can be very useful. That being said, if you fall into that category you’d earn status quicker by what you’re already doing than through this credit card.

It’s also worth noting that this card gives you Pearl status, but it doesn’t give you the 25,000 Tier credits needed for that status so you’d still need to earn 75,000 tier credits for gold and 200,000 for Platinum.

The one benefit that is intriguing is the annual free complimentary cruise with Royal Caribbean. For Platinum members this is actually the following:

3, 4 or 5-Night Bahamas or Caribbean cruise in an Oceanview Stateroom per year OR (1) $375 or $750 Cruise Fare Credit towards a new booking on any Royal Caribbean International cruise per year. Length of complimentary cruise and amount of Cruise Credit is based on guests recent M life play

If you earned Platinum status entirely from spend on this credit card you’d obviously get the shortest 3 night trip or a $375 cruise fare credit. I’m not even entirely sure if you would be eligible for this benefit considering this other ine print:

Guest must have earned M life tier through spend with MGM Resorts International

Now that hotels/resorts on the strip are starting to all charge for parking on the strip, people might be interested in this no annual fee card purely for the pearl status it comes with and the free parking associated with pearl status. I’d question how often you’d actually use that benefit, if you’re staying in Vegas most things on the strip are walking distance (and you wouldn’t want to self drive anyway).

The sign up bonus isn’t anything special, at most you’re getting $100 in value and there are plenty of credit cards with a higher cash bonus than that. None of the bonus spending categories are interesting either, with other cards offering better rebates. Personally I don’t see a lot of value in this card.

One last thing to keep in mind is that First National Bank of Omaha is not one of the larger credit card issuers, but they are somewhat inquiry sensitive.